JPMorgan ’s chief executive, Jamie Dimon, comment underscored how deeply AI is already embedded in mainstream corporate infrastructure. The bank employs more than 2,000 specialists and invests about $2 billion a year in AI yielding a comparable $2 billion in measurable annual savings through automation of risk, fraud detection, marketing, and client service. “It’s the tip of the iceberg,” Dimon said. “We’re getting better and better at it … our managers and leaders have to learn how to use this thing.”

The intention behind his remarks is that AI is no longer an R&D experiment but a productivity driver at scale, and that adoption is now spreading across every major financial and industrial enterprise.

Still, this optimism mirrors previous bubbles. In the late 1990s, investors built fibre networks far faster than end-user demand justified. Eventually the capacity was absorbed, but only after a painful correction. The same dynamic may now apply to GPUs and data centres. Capital is being deployed in anticipation of use-cases that have yet to prove durable economics.

The Market Psychology Behind AI Valuations

Market enthusiasm tends to overcorrect on both sides. In the late 1990s, investors overbuilt the internet’s physical layer — laying down massive fibre networks long before real demand materialised. Eventually, that capacity was used, but only after a painful correction. The same could apply today: billions are being deployed into data centres, GPU clusters, and AI startups under the assumption that compute demand will soon match supply. Investors understand the risk, but the logic of momentum and competition drives a form of collective overconfidence. No fund wants to be the one that missed “the obvious trade.” In this environment, capital deployment becomes a signalling exercise — a race to prove conviction. As in previous cycles, exuberance and peer pressure can override rational capital allocation, at least temporarily.Historical Echoes: The Dot-Com and Post-COVID Parallels

We’ve seen similar cycles before. The dot-com boom overbuilt infrastructure. The 2008 financial crisis was fuelled by over-leverage in real estate and the related mortgage market. And during the COVID lockdowns, record liquidity drove the SPAC and meme stock mania. Each cycle was followed by a sharp correction. When we look at the charts of how severe these corrections were and how long they lasted, it might look like each correction period was shortening. Like the market wash the excess quicly and moves back to the long-term trend of higher highs. But the effect in the real world out of the trading floor might take a bit longer to recover. After 2008, property bubbles and fragile banks in Spain, Greece, and Italy took years to unwind. Balance sheets were rebuilt through bailouts, recapitalisations, and painful restructuring before confidence returned. Today’s AI market could be following a similar script, with compute playing the role of property or fibre — the critical infrastructure of a digital future still taking shape.Are We Witnessing One of the Historicoal Bubbles?

Since the release of ChatGPT in November 2022, Nvidia’s market capitalisation has multiplied several-fold, transforming GPUs into the new oil of the digital economy.

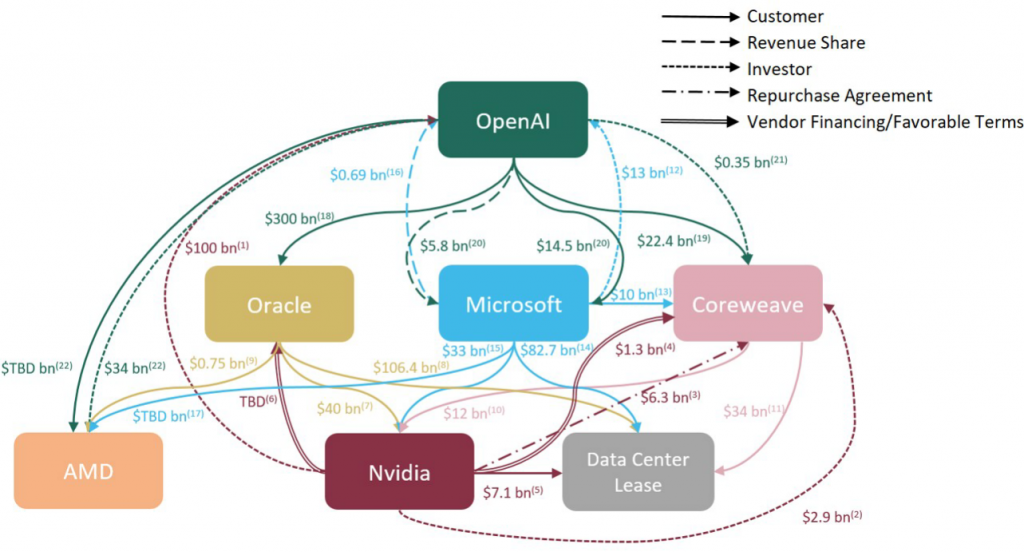

Recent partnerships — between OpenAI, Nvidia, AMD, Oracle, and even secondary players like CoreWeave — have created what analysts are now calling the “Circular AI Economy.” In just a few months, the industry’s largest companies have entered a dense web of reciprocal deals: OpenAI agreeing to purchase tens of billions of dollars’ worth of AMD chips while taking a stake in AMD itself; Nvidia investing up to $100 billion in OpenAI to co-develop new data-centre infrastructure; and OpenAI committing nearly $300 billion to run its workloads on Oracle’s cloud. Each agreement feeds the next — capital, chips, and compute flowing in a closed circuit that sustains valuation momentum across the same handful of firms.

Morgan Stanley recently published a report titled “AI: Mapping Circularity,” which examines how companies at the center of the AI boom — including OpenAI — are increasingly tied together through mutual funding, shared revenue, and cross-ownership. The report highlights that suppliers are now financing their own customers, blurring traditional market boundaries and creating a highly interconnected ecosystem. The following chart from Morgan Stanley illustrates this circular flow of capital and dependency surrounding OpenAI and its major partners.

Source: Company Data, Morgan Stanley Research.

Larry Ellison, who owns about 41% of Oracle, saw his fortune climb by approximately US $100 billion to US $392.6 billion (Forbes, Sept 2025). Elon Musk remains ahead at US $439.9 billion, but the gap has narrowed considerably.