Warranty liabilities capture the expected future cost of repairing or replacing products already sold under warranty terms. They are recorded as provisions so that the cost of honouring those commitments is recognised in the same reporting period as the related revenue, which gives management, investors, and acquirers a more reliable view of operating performance.

Definition

Warranty Liabilities

Estimated obligations for future warranty claims arising from goods already sold, recognised as a provision on the balance sheet when a probable outflow can be measured reliably.

What it means

A warranty liability reflects the estimated future cost of fulfilling repair and replacement promises attached to products already delivered to customers.

Recognition standard

Under IAS 37, the provision is recognised when the sale creates a present obligation, an outflow is probable, and the amount can be estimated reliably. The nearest US GAAP reference is ASC 460.

How it is calculated

Companies usually estimate the provision from historical claims rates, expected defect volumes, average repair costs, and the remaining warranty term across products in the market.

Why analysts care

If a provision is too low, current earnings look stronger than they really are, while future periods absorb the catch-up charge when claims arrive.

Valuation relevance

In M&A, an understated warranty provision is often treated as debt-like because the buyer will bear the cash cost of claims after closing.

Table of Contents

What Are Warranty Liabilities

A warranty liability is a provision recognised for the expected cost of honouring warranty commitments attached to products already sold. Under IAS 37, recognition is required when the sale has created a present obligation, a future outflow of resources is probable, and the company can estimate the amount with reasonable reliability. For businesses reporting under US GAAP, ASC 460 addresses guarantee-related obligations using broadly similar logic.

The accounting purpose is straightforward because accrual reporting aims to match cost with the revenue that generated it. When a company books the full sales margin today but waits to recognise repair and replacement costs until claims are submitted, reported profit in the sale period becomes artificially high. Recognising the provision at the point of sale corrects that timing distortion and makes the financial statements more useful for analysis.

Warranty provisions also sit within broader corporate finance analysis because they affect earnings quality, working capital interpretation, and balance sheet credibility. A provision that is consistently too low may signal weak forecasting discipline, product quality issues, or pressure to protect short-term profit.

How Warranty Liabilities Work

At each reporting date, management estimates the warranty cost likely to arise from units already sold and still covered. That estimate normally draws on historical claims data, defect rates by product line, average repair or replacement cost, labour and logistics inputs, and the remaining length of warranty coverage. Where recent design changes or supplier issues have altered product risk, historical averages need adjustment or they quickly become misleading.

The initial entry charges warranty expense in the income statement and credits a warranty provision on the balance sheet. When actual claims are processed, the cash cost is charged against the provision rather than against current-period profit. That treatment matters because it separates the cost of current sales from the settlement of obligations created in earlier periods.

Over time, the movement in the provision becomes highly informative. If actual claims repeatedly exceed the opening balance, the estimation method is too optimistic and prior-period earnings were overstated. If claims consistently run below the provision, management may be carrying excess reserves that flatter future profit when they are released.

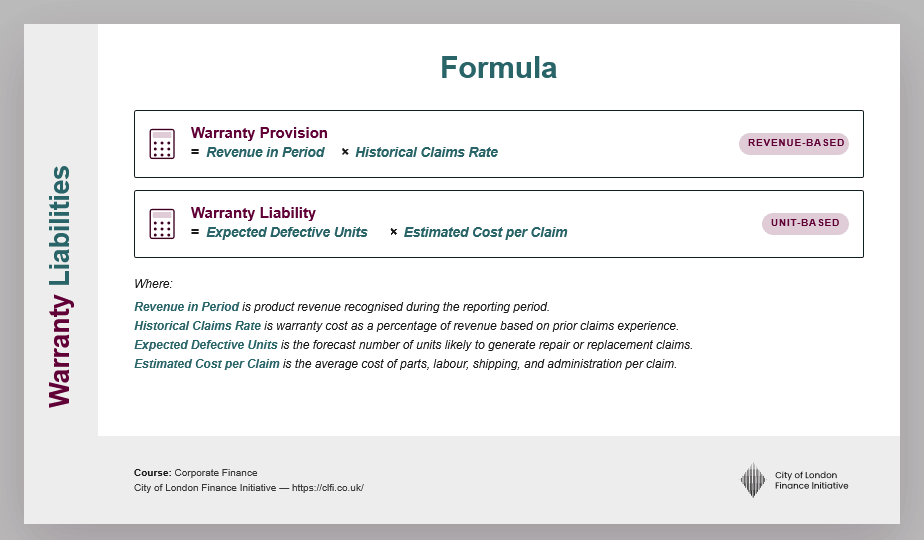

Warranty Liability Formula

Two common estimation approaches used in reporting and analysis

Revenue-based approach

Warranty Provision = Revenue in Period × Historical Claims Rate

Unit-based approach

Warranty Liability = Expected Defective Units × Estimated Cost per Claim

Definitions

Revenue in Period

Product revenue recognised during the reporting period.

Historical Claims Rate

Warranty cost as a percentage of revenue based on prior claims experience and current expectations.

Expected Defective Units

Forecast number of units likely to generate repair or replacement claims.

Estimated Cost per Claim

Average cost of parts, labour, shipping, and administration for each claim.

Formula and Calculation

Many businesses start with a revenue-based model because it is efficient and works well when claims behaviour is stable across periods. More operationally detailed businesses often prefer a unit-based model because it captures product-level differences in defect rates and repair costs. The stronger method depends on what the business sells and how much granular claims data it can trust.

Assume a manufacturer records £10,000,000 of product revenue in the period and historical warranty claims settle at 2 percent of revenue. The estimated provision is therefore £200,000. The journal entry records warranty expense of £200,000 in the income statement and a warranty provision of £200,000 on the balance sheet.

If actual claims in the next period amount to £165,000, that amount is charged against the provision, leaving £35,000 outstanding. That closing balance matters because it tells analysts whether the provision was prudent, aggressive, or broadly accurate once real claims begin to emerge.

Real-World Example

Consider a consumer electronics manufacturer with annual revenue of £50,000,000 and a standard two-year warranty. Using a historical claims rate of 1.8 percent, management records a warranty provision of £900,000 at year-end. During due diligence, however, a buyer finds that actual claims in the prior year ran at 2.3 percent of revenue, which implies a more realistic liability of £1,150,000 and a likely shortfall of £250,000.

| Item | Amount |

|---|---|

| Annual product revenue | £50,000,000 |

| Provision recorded at 1.8 percent | £900,000 |

| Implied liability at 2.3 percent | £1,150,000 |

| Potential understatement | £250,000 |

That gap matters beyond accounting presentation because the buyer expects to fund the excess claims after closing. In practice, the shortfall is often treated as debt-like in the enterprise value to equity bridge, while unusually high one-off warranty costs may also affect how advisers normalise EBITDA. The result is a lower equity value unless the seller can justify the original estimate with credible evidence.

Warranty Liability Compared with Contingent Liability

The distinction between a warranty liability and a contingent liability determines whether an obligation appears on the balance sheet or only in note disclosure. Warranty claims on goods already sold usually satisfy the IAS 37 recognition test because the obligation exists and a probable outflow can be estimated. Contingent liabilities sit outside the balance sheet when the outflow is only possible or the amount cannot yet be measured reliably.

| Feature | Warranty Liability | Contingent Liability |

|---|---|---|

| Balance sheet treatment | Recognised as a provision | Disclosed in notes only |

| Probability of outflow | Probable | Possible or uncertain |

| Measurement | Reliable estimate required | Reliable estimate not required for note disclosure |

| Income statement effect | Expense recognised with the sale | No expense unless recognition threshold is later met |

| Transaction impact | Often treated as debt-like in valuation bridges | Often addressed through deal protections and diligence |

Misclassifying the obligation changes both the balance sheet and the valuation story. If a probable warranty obligation is left in the notes as merely contingent, equity appears stronger than it should. If an uncertain obligation is recognised too early, current earnings become unnecessarily volatile. The classification decision therefore affects accounting quality and transaction pricing at the same time.

Key Considerations and Limitations

Warranty provisions are only as good as the assumptions behind them. Historical claims data may offer a solid starting point, though it loses reliability quickly when product design changes, suppliers fail, customer use shifts, or warranty terms are extended to defend market share. In each case, the past stops being a clean guide to future settlement cost.

Management incentives also matter because the provision affects reported profit before any cash leaves the business. A lower estimate lifts earnings immediately, while the shortfall may only become visible several reporting periods later when claims consistently draw down the reserve faster than expected. That is why analysts track provision roll-forwards rather than relying only on the closing balance.

There are further complications where warranty exposure overlaps with recalls, litigation, or consumer protection obligations across multiple jurisdictions. Those costs may not all sit within the standard warranty provision, and exchange rate movements can distort the apparent adequacy of a single consolidated number in international groups. Judgement therefore remains central even when the calculation itself looks simple.

In Practice

Warranty liabilities matter because they connect product quality, accounting judgement, and enterprise value in a single line item. For management, the real task is to estimate the provision using assumptions that reflect current operating conditions rather than stale averages. For analysts and buyers, the more useful question is whether the reserve has been calibrated honestly enough to withstand the actual pattern of claims now emerging.

Read alongside working capital trends, earnings adjustments, and valuation bridges, warranty provisions become more than a compliance exercise. They show whether reported profits are being supported by disciplined forecasting and whether future cash outflows have already been recognised where they belong. That is why provision adequacy remains a routine focus in financial reporting analysis and deal execution.

Programme Content Overview

The Executive Certificate in Corporate Finance, Valuation & Governance delivers a full business-school-standard curriculum through flexible, self-paced modules. It covers five integrated courses — Corporate Finance, Business Valuation, Corporate Governance, Private Equity, and Mergers & Acquisitions — each contributing a defined share of the overall learning experience, combining academic depth with practical application.

Chart: Percentage weighting of each core course within the CLFI Executive Certificate curriculum.