Shareholders' equity measures the residual interest that owners hold in a company after liabilities have been deducted from assets. It sits at the centre of balance sheet analysis because it shows how much of the business is financed by shareholders and how much value remains after creditor claims have been met.

Definition

Shareholders' Equity

The residual ownership claim on a company's assets after total liabilities have been deducted, as recorded in the equity section of the balance sheet.

What It Measures

Shareholders' equity shows the residual value of assets after liabilities, which means it represents the book value attributable to owners on the balance sheet.

Component Build-Up

The figure can also be built from share capital, share premium, retained earnings, and other comprehensive income, with treasury stock deducted where buybacks have reduced reported equity.

Primary Limitation

Because book equity is grounded in accounting rules and historical cost, it often understates economic value in businesses where brands, technology, or customer relationships drive performance.

Who Uses It

Analysts, finance leaders, and investors use shareholders' equity in return on equity, book value per share, capital structure analysis, and the equity starting point for enterprise value work.

Why The Distinction Matters

Shareholders' equity captures the ownership claim only, while enterprise value extends beyond equity by incorporating debt and cash adjustments when the whole business is being valued.

Table of Contents

What Is Shareholders' Equity

Shareholders' equity is the residual ownership interest in a company's assets after all liabilities have been deducted. Within the balance sheet equation, assets are funded either by obligations to creditors or by capital attributable to owners, so equity acts as the balancing figure that completes the capital structure recorded in the accounts.

That accounting role matters because the equity section preserves the financial history of the business. It records capital contributed through share issuances, profits retained instead of distributed, gains and losses recognised outside the income statement, and the effect of buybacks that reduce reported equity when shares are repurchased from the market. This is why the line connects directly with wider questions of corporate finance, capital structure, and value creation.

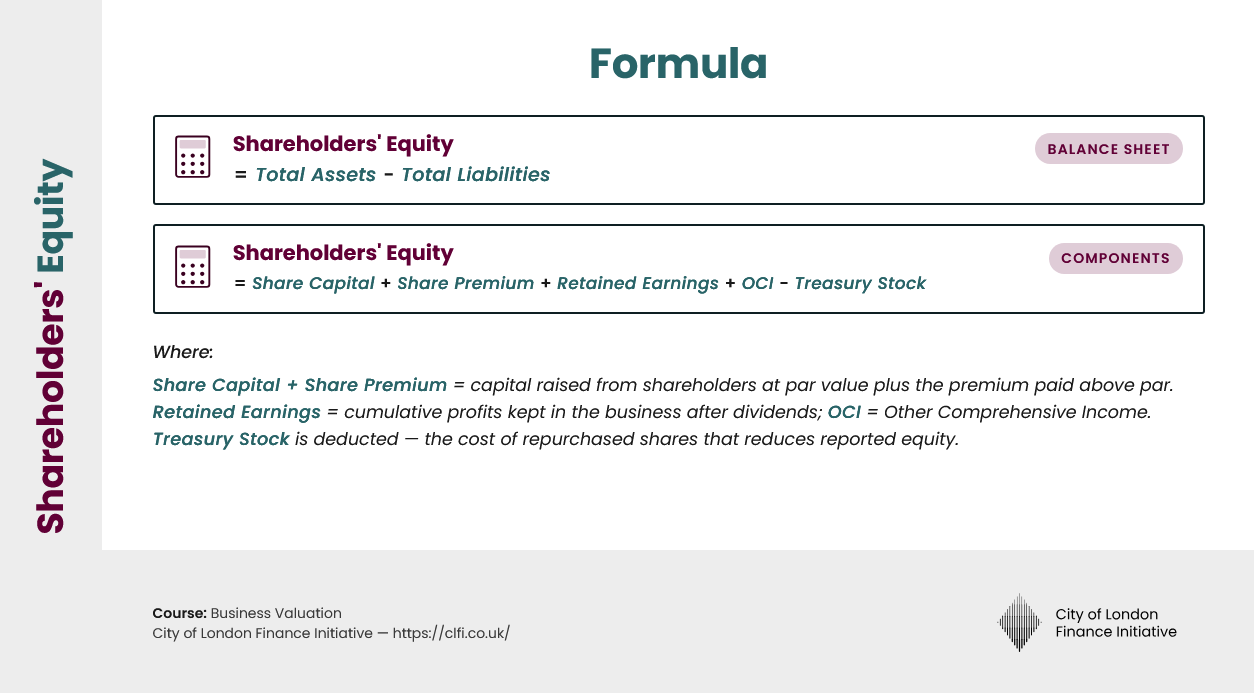

Shareholders' Equity Formula

Balance sheet method and component method

Balance sheet method

Shareholders' Equity = Total Assets - Total Liabilities

Component method

Shareholders' Equity = Share Capital + Share Premium + Retained Earnings + Other Comprehensive Income - Treasury Stock

Definitions

Share Capital

Par value of shares in issue.

Share Premium

Amount received above par value when shares are issued.

Retained Earnings

Cumulative profits kept in the business after dividends.

Other Comprehensive Income

Gains and losses recognised outside the income statement.

Treasury Stock

Cost of repurchased shares deducted from equity.

Interpretation

Both methods should produce the same number, though the component view explains how the balance evolved.

Worked Example

Assume Clearwater Holdings reports total assets of £620 million and total liabilities of £395 million. The balance sheet method therefore produces shareholders' equity of £225 million. Rebuilding the figure from the equity section arrives at the same result, though it also reveals that retained earnings have been the main source of book value while buybacks have reduced the headline balance.

| Balance Sheet Item | £ million |

|---|---|

| Total Assets | 620 |

| Total Liabilities | 395 |

| Shareholders' Equity | 225 |

| Equity Component | £ million |

|---|---|

| Share Capital | 40 |

| Share Premium | 85 |

| Retained Earnings | 145 |

| Other Comprehensive Income | 15 |

| Treasury Stock Deduction | (60) |

| Shareholders' Equity | 225 |

The example shows why the component view matters. Retained earnings of £145 million point to years of profitable operation, while the £60 million treasury stock deduction shows that buybacks have compressed reported equity even though the business may still be financially strong. For an executive reviewing capital allocation, that distinction prevents a mechanical reading of the headline number.

Key Considerations and Limitations

Shareholders' equity is reliable as an accounting identity, though it is an imperfect proxy for economic worth. Historical cost rules leave many internally generated intangibles off the balance sheet, so companies built on software, brands, data, or customer relationships can look understated on a book basis even when their competitive position is exceptionally strong.

Acquisitions can create the opposite effect because purchase premiums appear through goodwill and other acquired intangibles. Reported equity may therefore rise even when the underlying tangible asset base has changed only modestly. Negative book equity also needs interpretation rather than alarm, since sustained buybacks or repeated special distributions can drive the figure below zero without implying immediate distress.

In analysis, the equity line works best as a starting point. It should be tested against cash generation, leverage, return on equity, and valuation measures that reflect the business as a whole. That broader view matters because a single accounting figure cannot capture operating quality, market expectations, or strategic optionality on its own.

In Practice

Shareholders' equity remains one of the most useful balance sheet measures because it links ownership, capital structure, and accounting performance in a single line. Yet its real value comes from interpretation rather than extraction. Executives who read the number well look past the headline balance and ask how much of it comes from retained profit, how much reflects external funding, how much has been reduced by buybacks, and how far accounting value may sit from economic value.

Used in that way, shareholders' equity becomes more than a book figure. It helps frame return on equity, acquisition bridges, funding decisions, and the quality of capital allocation over time. That makes it a practical starting point for board-level judgement, especially when it is paired with cash flow analysis, leverage assessment, and valuation measures that capture the full economics of the business.

Equity Analysis Becomes Stronger When Valuation Context Is Added

Shareholders' equity, enterprise value, and valuation bridges are examined in the Business Valuation Executive Course, which connects accounting measures with market-based analysis and transaction judgement.

Programme Content Overview

The Executive Certificate in Corporate Finance, Valuation & Governance delivers a full business-school-standard curriculum through flexible, self-paced modules. It covers five integrated courses — Corporate Finance, Business Valuation, Corporate Governance, Private Equity, and Mergers & Acquisitions — each contributing a defined share of the overall learning experience, combining academic depth with practical application.

Chart: Percentage weighting of each core course within the CLFI Executive Certificate curriculum.