Carried interest is the mechanism through which a private equity or hedge fund manager shares in the returns generated for investors. It rewards performance rather than activity, distributing a portion of profits to the General Partner only after Limited Partners have recovered their capital and received an agreed minimum return. Understanding how carry is structured, calculated, and distributed is essential for anyone operating within or alongside private fund structures.

Definition:

Carried Interest

The share of investment profits allocated to a private equity or hedge fund manager as performance compensation, calculated as a percentage of returns above an agreed hurdle rate and paid only after Limited Partners have recovered their invested capital.

- What it means: The GP's performance share of fund profits, earned only above the hurdle rate.

- Standard terms: 20% of profits above an 8% preferred return, distributed after LP capital is returned in full.

- Alignment mechanism: Carry defers GP compensation until investors are made whole, linking incentives directly to realised returns.

- Key protection: Clawback provisions require GPs to return carry if later investments erode earlier gains within the same fund.

- Tax complexity: In most jurisdictions carry is treated as a capital gain rather than income, a classification that has attracted sustained regulatory scrutiny.

Table of Contents

Definition

Carried interest is the performance allocation paid to the General Partner of a private fund once investment returns exceed a specified threshold, known as the hurdle rate or preferred return. It operates as the primary mechanism through which GPs share in the upside they generate for the fund's investors. The term originates from the historical practice of ship merchants receiving a "carry" (a share of cargo profits) for transporting goods on behalf of investors. In contemporary private markets, it forms the cornerstone of the GP/LP incentive structure, ensuring that fund managers are compensated in direct proportion to the value they create rather than simply the capital they manage.

How Carried Interest Works

Private equity and venture capital funds are structured as limited partnerships, with LPs contributing capital and GPs managing it. Carried interest governs how profits are shared once the fund achieves its agreed return threshold, following a distribution waterfall that sequences payments in a defined order.

The waterfall begins with a full return of LP capital, followed by the preferred return, typically 8% per year on unreturned capital. Once LPs have received both, remaining profits are divided between the GP and LPs, with the GP receiving carry of approximately 20% and LPs retaining the remaining 80%. In some fund structures, a GP catch-up provision applies, allowing the GP to receive a temporarily higher proportion of distributions until carry reaches the agreed percentage of total fund profits across all periods.

The hurdle rate acts as the minimum acceptable return investors must receive before the GP participates in any upside, and it is closely related to the concept of internal rate of return (IRR), which funds use to measure performance against that threshold. Because carry is earned at the back end of a fund's life, often after a five-to-ten-year investment horizon, it creates a strong incentive for GPs to maximise realised returns rather than unrealised paper valuations.

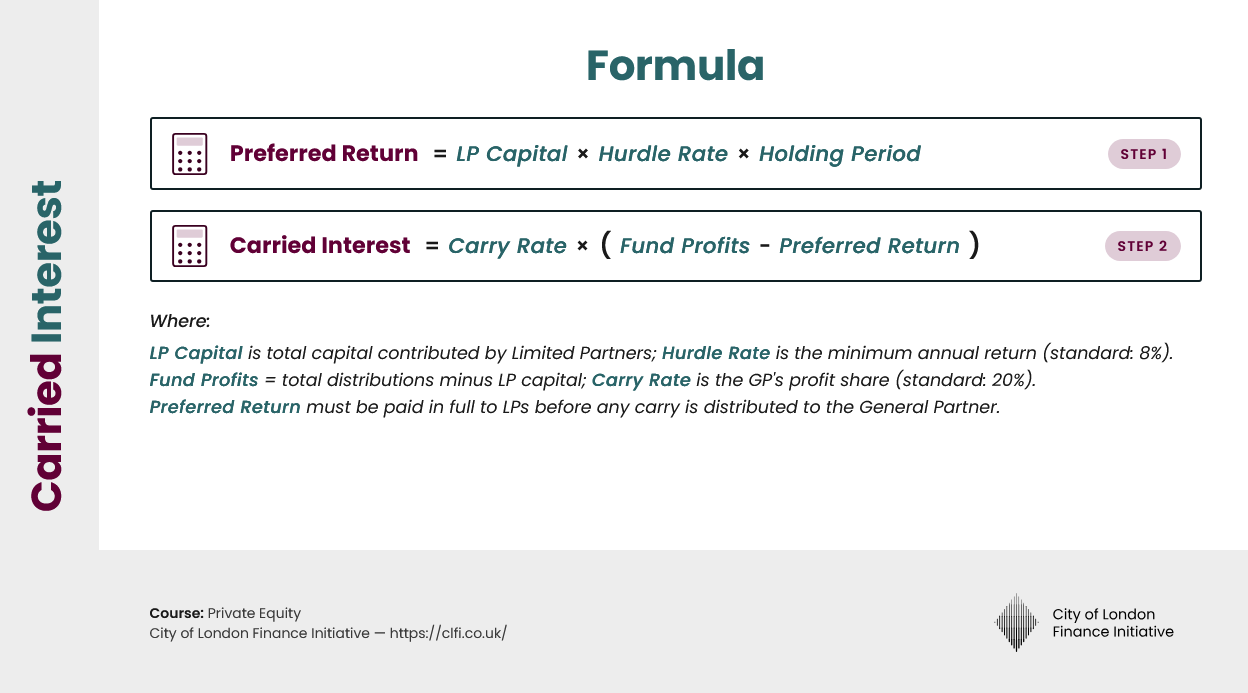

Carried Interest Formula

Formula, variable definitions, and worked example

Formula

Carried Interest = Carry Rate × (Total Fund Profits − Preferred Return)

Variable Definitions

Carry Rate

The agreed percentage of profits allocated to the GP. Market standard is 20%.

Total Fund Profits

Total distributions to all investors minus total LP capital contributed.

Preferred Return

LP capital contributed × hurdle rate × holding period (annualised). Typically 8% per annum.

Hurdle Rate

The minimum annual return LPs must receive before the GP participates in profits. Standard rate: 8%.

Worked Example

A private equity fund raises £500 million from LPs. After a 7-year hold period, the fund distributes £900 million in total.

| Step 1 | Total profit = £900m − £500m = £400m |

| Step 2 | Preferred return (8% p.a. simple, 7 years) = £500m × 8% × 7 = £280m |

| Step 3 | Profits above hurdle = £400m − £280m = £120m |

| Step 4 | Carry at 20% = £120m × 20% = £24 million |

The GP receives £24m in carried interest. LPs receive the remaining £96m in profits above the hurdle, plus their £280m preferred return, plus their original £500m capital returned.

Real-World Example: Blackstone and Hilton Hotels

The 2007 leveraged buyout of Hilton Hotels by Blackstone Group is frequently cited as one of the most profitable carry events in private equity history. Blackstone acquired Hilton for approximately $26 billion, steered the company through the financial crisis, and took it public in 2013. By the time Blackstone fully exited its position in 2018, the fund had generated estimated returns of over $14 billion on equity invested of approximately $5.5 billion, a multiple that placed it among the largest single-asset profit events the industry had seen.

The carry allocation arising from this single investment contributed substantially to GP economics across the fund's entire life, illustrating a broader principle about how carry actually works in practice. A single large exit can determine whether a vintage year is transformative or modest for both partners, because carry accrues on a fund-wide basis and one exceptional realisation can tip the entire waterfall in the GP's favour. This is why GPs devote disproportionate attention to their largest positions throughout the hold period, and why LPs negotiating fund terms pay close attention to how carry is calculated across individual deals versus the aggregate portfolio.

Key Considerations and Limitations

The back-end nature of carry creates a timing asymmetry that practitioners must account for carefully. GPs benefit most from long holding periods and large exits, which may not always align with the interests of LPs who prefer earlier liquidity or a more distributed return profile across the fund's life. In funds without robust clawback provisions, early profitable exits can result in GPs retaining carry that is later eroded by losses on subsequent investments within the same fund, leaving LPs in a position where they have effectively overpaid for performance that was not sustained.

The hurdle rate is frequently calculated on a fund-wide basis rather than deal by deal, which means strong performance in early investments can effectively subsidise underperforming assets held later in the cycle. Tax treatment also varies significantly by jurisdiction. In the United Kingdom, HMRC has progressively tightened its rules on carry classification, while in the United States the treatment of carry as capital gains rather than ordinary income remains a contested policy debate. These structural and regulatory complexities mean that the true economics of any given carry arrangement require careful modelling before a fund closes, and executives reviewing fund terms should not assume that standard market conventions apply uniformly across geographies or fund vintages.

Carried Interest vs Management Fee

Management fees and carried interest together form the "2 and 20" structure that defines most institutional private fund compensation, but they serve fundamentally different purposes. The management fee is charged regardless of performance, typically 1.5 to 2 percent per annum on committed or invested capital, and covers the GP's operating costs across the fund's life. Carried interest, by contrast, is contingent on results above the hurdle and is distributed only after LPs are made whole, which is why understanding how private equity fees are structured provides important context for evaluating the full cost and incentive design of any fund arrangement.

| Feature | Carried Interest | Management Fee |

|---|---|---|

| Basis | Percentage of profits above the hurdle | Percentage of committed or invested capital |

| Typical rate | 20% of profits above 8% hurdle | 1.5% to 2% per annum |

| Contingency | Earned only if performance threshold is met | Charged regardless of performance |

| Purpose | Aligns GP incentives with LP returns | Covers GP operating costs |

| Timing | Distributed at exit or end of fund life | Charged annually throughout fund life |

Fund Mechanics. GP Economics. Executive Perspective.

Learn more through the Executive Certificate in Corporate Finance, Valuation & Governance — covering private equity fund structure, GP/LP incentives, and value creation from an executive perspective.

Conclusion

Carried interest is best understood not as a fee but as an alignment mechanism, one that defers GP compensation until the fund has delivered real returns to its investors. The 20% carry standard has remained largely unchanged for decades because it reflects a practical equilibrium between the risk GP management teams absorb over a fund's life and the upside they share with LPs once that risk pays off.

For executives sitting on investment committees, reviewing fund terms, or managing relationships with PE-backed portfolio companies, understanding the carry structure matters because it directly shapes the decisions GPs make throughout a fund's investment cycle. A GP approaching the end of a fund's life with unrealised carry will behave differently from one whose carry has already vested, and those behavioural incentives have real consequences for valuations, exit timing, and post-acquisition management priorities.

Reading carry terms alongside clawback provisions, hurdle structures, and distribution waterfalls gives executives the analytical foundation to evaluate fund economics with the same rigour they would apply to any other capital allocation decision. Carry is not simply an expense line in a fund relationship. It is the governing logic behind how your GP thinks, what they prioritise, and when they will act.

Programme Content Overview

The Executive Certificate in Corporate Finance, Valuation & Governance delivers a full business-school-standard curriculum through flexible, self-paced modules. It covers five integrated courses — Corporate Finance, Business Valuation, Corporate Governance, Private Equity, and Mergers & Acquisitions — each contributing a defined share of the overall learning experience, combining academic depth with practical application.

Chart: Percentage weighting of each core course within the CLFI Executive Certificate curriculum.