Mergers and acquisitions, commonly referred to as M&A, describe the transactions through which companies combine, purchase one another, or restructure ownership to pursue growth, generate synergies, or reposition strategically. M&A activity sits at the intersection of corporate finance and corporate strategy, driven by investment banks, legal advisers, boards, and management teams working under significant time and financial pressure.

Definition

Mergers and Acquisitions (M&A)

Corporate transactions in which companies combine (merger) or one company purchases another (acquisition) to create value through synergies, accelerate growth, acquire capabilities, or reshape competitive positioning. M&A encompasses the full deal lifecycle, covering strategic rationale and valuation, due diligence, regulatory approval, negotiation, and post-merger integration.

Table of Contents

- What Are Mergers and Acquisitions?

- Types of M&A

- Why M&A Happens

- The M&A Process: From Mandate to Close

- Due Diligence in M&A

- Valuation Methods for M&A

- Hostile Takeovers and Bid Defence

- Regulatory Approval and Antitrust Review

- Cross-Border M&A

- Post-Merger Integration (PMI)

- Limits and Risks of M&A

- Case Study: Google’s Acquisition of YouTube

- Frequently Asked Questions

What Are Mergers and Acquisitions?

A merger occurs when two companies agree to combine and form a single entity, usually to strengthen their market position, achieve economies of scale, or accelerate entry into new markets. An acquisition happens when one company purchases another and assumes control. The target becomes a subsidiary or is absorbed entirely into the acquirer’s operations. Although often grouped together, mergers and acquisitions differ in structure, strategic logic, and perception.

That distinction matters in theory, but in practice the line is often blurred. The merger of Essilor and Luxottica created a global eyewear leader through a combination of equals, while Microsoft’s acquisition of LinkedIn was a straightforward purchase that brought the target under Microsoft’s full control. Investment banks play a central role in both types of transaction, advising buyers and sellers on strategy, valuation, deal structure, and negotiation. This is a process that can span months and require teams of lawyers, accountants, and financial advisers working in parallel.

Whatever form a deal takes, M&A activity as a whole is cyclical, typically rising during periods of low interest rates, strong equity markets, and high corporate confidence, and contracting when credit tightens or uncertainty increases. At its core, every M&A transaction is a bet on the future: that the combined entity will be worth more than the sum of its parts, and that the acquirer can execute integration without destroying the value the target already possesses.

Types of M&A

M&A transactions take different forms depending on strategic objectives. Each type has different implications for growth, control, integration complexity, and risk:

- Horizontal merger: Two companies operating in the same industry and often as direct competitors combine. This type of merger is typically pursued to increase market share, achieve economies of scale, and reduce competition. Airline consolidations, for example, allow carriers to share routes, reduce overlapping costs, and strengthen pricing power.

- Vertical merger: Companies at different stages of the supply chain join together. A vertical merger can be backward (a company acquires a supplier or manufacturer to secure critical inputs) or forward (a company acquires a distributor or retailer to reach customers more directly). The main objectives are efficiency, cost reduction, and tighter control over production and distribution.

M&A Course Module 1.3 Type of Mergers - Conglomerate merger: A transaction between companies in unrelated industries. The purpose is diversification: spreading risk across sectors or allocating surplus capital into new growth areas. While conglomerates can create stability by reducing dependence on a single market, they often face challenges in managing diverse business units with little operational overlap.

- Acquisition of control: One company purchases a controlling stake of more than 50% in another company. Unlike a merger of equals, control acquisitions allow the buyer to integrate operations, redirect strategy, or capture specific assets such as technology or brands. This route is common in cross-border deals where firms seek access to new markets without building from scratch.

- Leveraged buyout (LBO): An acquisition financed primarily with borrowed funds, where the target’s assets and cash flows are often used to secure and repay the debt. LBOs are a hallmark of private equity, allowing investors to amplify returns through leverage. However, they also increase financial risk, making post-acquisition cash generation and operational improvement critical to success.

Why M&A Happens

The motivations behind M&A vary, but most transactions are driven by a combination of synergies, growth objectives, strategic repositioning, and financial opportunity. Understanding these drivers helps explain why some deals create lasting value while others struggle to deliver on expectations.

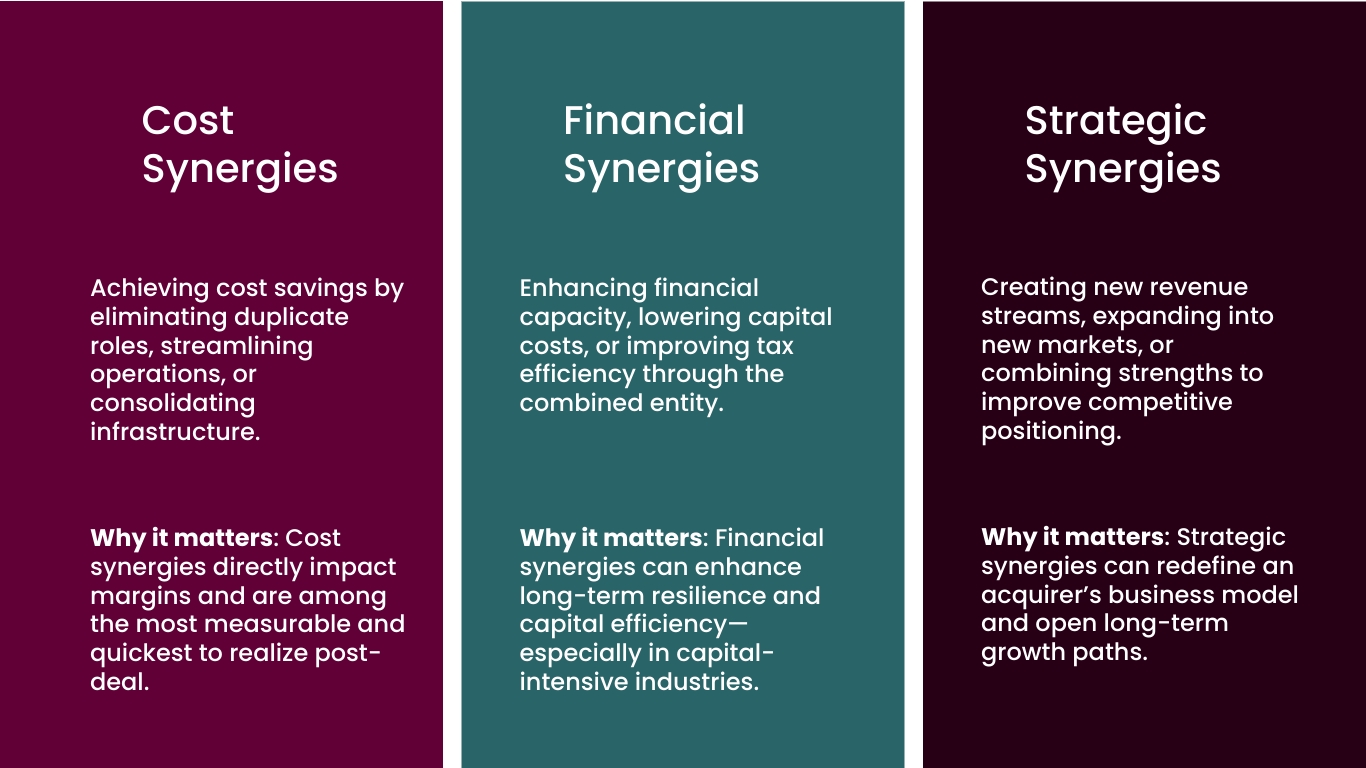

- Synergies: The most frequently cited reason for M&A, synergies capture the idea that the combined entity will be worth more than the sum of its parts. These are typically classified into three categories:

- Cost synergies: Achieved by eliminating duplicate functions, streamlining operations, or consolidating infrastructure. These directly improve profit margins and are often the quickest to realise after a deal closes.

- Financial synergies: Enhanced financial strength through lower cost of capital, increased borrowing capacity, or better tax efficiency. These synergies improve long-term resilience, especially in capital-intensive industries.

- Strategic synergies: Opportunities to generate new revenue streams, expand into new markets, or combine complementary strengths to improve competitive positioning. These are often the most transformative, shaping the long-term direction of the combined company.

M&A Course Module 1.4: Synergies in M&A - Growth: Acquiring another business can accelerate entry into new markets, product lines, or geographies, providing a faster route than organic expansion. A consumer goods company may acquire a regional brand to gain immediate distribution and brand recognition that would take years to build independently.

- Strategic repositioning: M&A can reshape a company’s future by adding new capabilities, technologies, or intellectual property. This type of transaction often reflects a response to disruptive change or the need to realign with market trends, such as acquiring AI or data analytics expertise in the technology sector.

- Financial motives: Some deals are pursued because of favourable financial conditions, including undervalued targets, low interest rates, or tax advantages. In these cases, acquirers see an opportunity to unlock value through timing and capital structure benefits rather than operational improvement alone.

Programme Content Overview

The Executive Certificate in Corporate Finance, Valuation & Governance delivers a full business-school-standard curriculum through flexible, self-paced modules. It covers five integrated courses — Corporate Finance, Business Valuation, Corporate Governance, Private Equity, and Mergers & Acquisitions — each contributing a defined share of the overall learning experience, combining academic depth with practical application.

Chart: Percentage weighting of each core course within the CLFI Executive Certificate curriculum.

The M&A Process: From Mandate to Close

A typical M&A transaction moves through a structured sequence of stages, each involving multiple advisers and escalating financial and legal commitment. Investment banks typically lead the process on behalf of either the buyer (buy-side mandate) or the seller (sell-side mandate), advising on strategy, managing information flow, and coordinating the bid process.

Key Stages of an M&A Transaction

- Strategy and target identification: The acquirer defines its M&A rationale and identifies potential targets that fit the strategic and financial criteria. Investment banks or internal corporate development teams screen candidates and prioritise the shortlist.

- Preliminary valuation and approach: A preliminary valuation is performed using publicly available data. If the target is private, the approach is made directly to the board or shareholders. Non-disclosure agreements (NDAs) are signed before any sensitive information changes hands.

- Letter of Intent (LOI) or Heads of Terms: If initial discussions progress, a non-binding letter of intent sets out the proposed deal structure, indicative price range, and exclusivity period. This formalises the acquirer's intent without creating binding financial commitments.

- Due diligence: A detailed examination of the target's financial, legal, commercial, and operational position. This is the phase where deal assumptions are tested and risks are quantified or mitigated.

- Negotiation and definitive agreements: Based on due diligence findings, the parties negotiate final deal terms including price, conditions precedent, representations and warranties, and any earn-out or indemnification provisions. Legal counsel drafts the definitive agreements (SPA or merger agreement).

- Regulatory approval and closing: Larger transactions require antitrust clearance from relevant authorities before closing. Once approvals are obtained and conditions are satisfied, the deal closes and consideration (cash, shares, or a combination) is exchanged.

Across all these stages, timelines vary considerably. A straightforward acquisition of a private company can close in three to six months, while a complex cross-border merger involving multiple regulatory jurisdictions may take twelve to eighteen months from announcement to completion.

Due Diligence in M&A

Due diligence is the structured investigation an acquirer conducts on a target company before committing to final deal terms. Its purpose is to verify the assumptions underpinning the valuation, surface risks that would affect the purchase price or deal structure, and identify any issues that could undermine value post-closing. Far from a formality, due diligence is where many deals are renegotiated and sometimes abandoned.

Due diligence is typically conducted across four parallel workstreams, each managed by specialist advisers and feeding findings back to the deal team and the acquirer's board:

Financial Due Diligence

Led by accountants or corporate finance advisers, financial due diligence examines the quality of the target's earnings, the sustainability of its cash flows, and the accuracy of its reported financial position. Key questions include: Are the revenues recurring or one-off? Have margins been maintained artificially? Are there off-balance-sheet liabilities, pension deficits, or contingent obligations that would alter the true cost of the acquisition? The output typically includes a Quality of Earnings (QoE) report that adjusts reported EBITDA to reflect normalised, sustainable performance that will form the basis for EV/EBITDA valuation multiples.

Legal Due Diligence

Legal advisers review contracts, intellectual property ownership, employment arrangements, litigation history, regulatory licences, and corporate governance. The goal is to identify any contractual provisions that could be triggered by a change of control (commonly known as "change of control clauses"), any pending or threatened litigation that could create post-closing liability, and any gaps in IP ownership or licensing arrangements that could affect the target's business model.

Commercial Due Diligence

Commercial due diligence tests the market assumptions behind the acquisition case. This includes analysing the target's competitive position, customer concentration, sales pipeline, pricing power, and the sustainability of its growth forecast. A target whose revenue is heavily concentrated in two or three customers presents a different risk profile from one with thousands of distributed accounts. That distinction has a direct bearing on the valuation multiple an acquirer should pay.

Operational Due Diligence

Operational due diligence assesses the target's systems, processes, technology infrastructure, and management team. It examines whether the operational platform is scalable, whether there are significant capital expenditure requirements not reflected in the financial projections, and whether key management talent is likely to remain post-acquisition. For private equity buyers executing an LBO, this workstream also informs the integration plan and the timeline for realising cost synergies.

For all the rigour these workstreams bring, the findings are rarely clean. Discovered issues, known as diligence findings, are typically addressed through price adjustments, escrow arrangements, representations and warranties insurance (RWI), or specific indemnities from the seller. In extreme cases, material findings can lead to deal termination. Buyers who conduct thorough due diligence before signing are substantially better positioned to integrate successfully and avoid post-closing disputes.

Valuation Methods for M&A

Valuing companies in M&A transactions is one of the most technically demanding aspects of corporate finance. It goes beyond financial modelling and requires understanding both the target's fundamental performance and the strategic rationale for the deal. Analysts and executives rely on several core methods, each offering a different perspective on value. Experienced deal teams use all of them together to triangulate a defensible price range.

- Discounted Cash Flow (DCF): Projects the target's future free cash flows and discounts them back to present value using the appropriate Weighted Average Cost of Capital (WACC). DCF captures the intrinsic value of a business based on its ability to generate cash over time, making it the most theoretically rigorous method. However, it is highly sensitive to assumptions about growth rates and the terminal value, which typically accounts for 60–80% of total value in a standard model. Small changes in the discount rate or the long-run growth assumption can shift the valuation by 20–30%, which is why DCF outputs are always presented as a range rather than a single figure.

- Comparable company analysis (trading comps): Benchmarks the target against similar publicly traded companies using multiples such as EV/EBITDA, EV/Revenue, or Price/Earnings. This method provides a "market view" of value rooted in how investors currently price comparable businesses. Its limitation is that no two companies are truly alike, and listed comparables trade without a control premium, meaning their multiples typically understate the value a strategic buyer would pay.

- Precedent transaction analysis (deal comps): Examines valuations paid in recent M&A transactions for comparable targets. This approach reflects real-world deal dynamics, including the control premiums buyers have historically paid in the sector. Precedent transactions are particularly useful for validating whether the proposed price is within the range that the market has accepted for similar assets.

- Premium and control analysis: Focuses on the additional price buyers are typically willing to pay above a target's unaffected share price to secure control, access synergies, or block a competitor from acquiring the asset. Control premiums in public M&A transactions have historically averaged 25–35% above pre-announcement trading prices, though they vary significantly by sector, deal type, and competitive dynamics in the auction process.

Learn how to apply these valuation methods step by step, and develop the practical tools to navigate real M&A transactions, in our Executive Certificate in Corporate Finance, Valuation & Governance.

Hostile Takeovers and Bid Defence

Not all M&A transactions are negotiated collaboratively. A hostile takeover occurs when an acquirer bypasses the target's board and makes its offer directly to shareholders, typically because the board has rejected the approach or is unwilling to engage. Hostile bids are more common in jurisdictions with active capital markets such as the United Kingdom and the United States, where public company shares are widely distributed and shareholders retain direct voting rights over deal acceptance.

When a bidder does go hostile, the most common mechanism is a tender offer, in which the acquirer offers to purchase shares directly from shareholders at a stated price for a fixed period. If enough shareholders accept (typically more than 50%), the acquirer obtains control regardless of the board's position. In the UK, hostile bids are regulated by the Takeover Code and supervised by the Takeover Panel, which sets strict rules around bid timetables, disclosure, and equal treatment of shareholders.

Facing this kind of pressure, target companies can deploy several defence mechanisms, including the poison pill (a shareholder rights plan that dilutes an acquirer's stake if it crosses a threshold), seeking a white knight (a preferred buyer willing to pay more on friendlier terms), or making the company operationally unattractive through a large acquisition or special dividend. In the UK, the Takeover Code limits some of these tactics, placing more power with shareholders than in many other jurisdictions.

Regulatory Approval and Antitrust Review

Larger M&A transactions typically require approval from one or more competition authorities before they can close. Regulators assess whether the proposed combination would substantially reduce competition in any relevant market. They can require divestitures, impose behavioural remedies, or block the transaction entirely if competitive harm cannot be addressed.

The principal regulatory bodies relevant to UK and international M&A include:

- Competition and Markets Authority (CMA): The UK's primary merger control authority. Since Brexit, the CMA reviews all deals meeting UK turnover thresholds independently of the European Commission, and has taken an increasingly assertive stance on large technology and healthcare mergers.

- European Commission (EC): Reviews mergers with an EU dimension under the EU Merger Regulation. Deals above specified turnover thresholds are reviewed at EU level, providing a "one-stop shop" for multi-country European clearance.

- Committee on Foreign Investment in the United States (CFIUS): Reviews foreign acquisitions of US businesses for national security implications. CFIUS has significantly expanded its scope in recent years, covering sensitive technology, critical infrastructure, and data-rich businesses. For cross-border deals involving US assets, CFIUS review has become a material deal risk.

Taken together, these frameworks make regulatory risk an increasingly important factor in M&A strategy. Deals that require divestiture conditions are typically worth less to the buyer than originally modelled, and deals that are blocked can expose both parties to significant advisory and opportunity costs. Pre-deal regulatory assessment, including informal dialogue with authorities before announcement, is now standard practice for large transactions.

Cross-Border M&A

Cross-border M&A, where the acquirer and target are based in different countries, introduces additional layers of complexity beyond those found in domestic transactions. Currency risk, differing accounting standards (IFRS versus US GAAP), multiple regulatory jurisdictions, tax treaty implications, and cultural differences in management practice and employee expectations all require careful management from the outset of the deal.

The appeal is usually pragmatic. Acquiring a local business is frequently faster and cheaper than building operations from the ground up in an unfamiliar jurisdiction. Yet the failure rate of cross-border deals is higher than for domestic transactions, primarily because cultural integration is harder to plan, execute, and measure than financial integration. Differences in employment law, union representation, and management communication norms can derail even a financially sound deal if they are not addressed early in the integration planning process.

Post-Merger Integration (PMI)

Post-merger integration is where the value promised in the deal rationale is either realised or destroyed. Research consistently shows that between 70% and 90% of M&A transactions fail to deliver the financial returns projected at the time of acquisition. The most common reasons are operational and cultural: failure to integrate systems in a timely manner, loss of key talent who leave during the uncertainty of transition, cultural clashes that undermine productivity, and synergy estimates that were never realistic to begin with.

Given the scale of that challenge, effective PMI must begin before the deal closes. Best-practice acquirers designate an integration management office (IMO) during the due diligence phase, staffed by senior leaders with clear decision-making authority. The IMO coordinates workstreams across finance, operations, HR, IT, legal, and communications, tracking synergy realisation against the deal model and managing the day-to-day decisions that determine whether the combined organisation functions effectively in the months after close.

The right model depends on where value is expected to come from. A full integration (where the target is absorbed entirely into the acquirer) maximises cost synergy potential but carries the highest execution risk and disrupts the target's business most severely. A standalone model (where the target continues to operate independently under new ownership) preserves the target's culture and customer relationships but limits cost synergies. Private equity firms executing an LBO, in particular, typically choose a model based on where value is expected to come from: operational improvement, financial engineering, or strategic repositioning.

Timing matters as much as structure. The first 100 days post-close are widely regarded as the critical integration window, and decisions made in this period, covering leadership appointments, systems migration priorities, communication to employees and customers, and the sequencing of cost reduction initiatives, set the trajectory for the entire integration. Acquirers that delay these decisions, or that understaff the integration effort, consistently underperform those that invest heavily in structured integration from day one.

Limits and Risks of M&A

Despite their promise, M&A deals frequently fail to deliver the anticipated returns. Integration challenges, cultural clashes, overestimation of synergies, excessive acquisition debt, and departure of key talent are among the most commonly cited causes of deal underperformance. Acquirers also face the risk of paying too much in competitive auction processes where the pressure to win overrides pricing discipline, resulting in goodwill impairment charges that reduce shareholder value for years after the deal closes.

The evidence consistently points to the same remedies. Valuation discipline, clear strategic rationale, rigorous due diligence, and structured post-merger integration planning are the four factors most consistently associated with M&A success. Deals motivated by competitive pressure ("we need to do something because our rival just did") or by the desire to deploy excess cash rather than a well-articulated strategic thesis are disproportionately represented among transactions that destroy value. The best acquirers treat M&A as one option among many, pursued only when the deal is the most efficient route to a specific strategic objective and the price can be justified under disciplined assumptions.

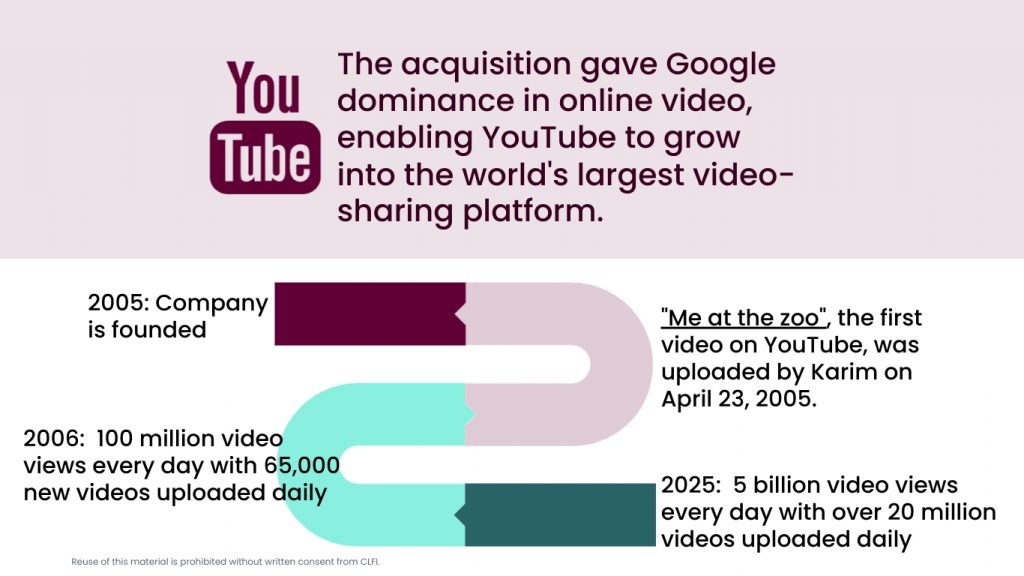

Case Study: Google's Acquisition of YouTube

In October 2006, Google announced it would acquire YouTube for $1.65 billion in an all-stock deal. At the time, YouTube was just 18 months old but already served 100 million video views per day with 65,000 daily uploads. Google recognised YouTube's potential to dominate online video and integrated it as a subsidiary while preserving its brand identity. The deal became one of the most successful technology acquisitions in history.

The numbers since tell their own story. In 2024 alone, YouTube generated $36.1 billion in advertising revenue. The platform now generates the equivalent of its original $1.65 billion purchase price every two weeks. For early investors and founders, the acquisition delivered extraordinary returns, demonstrating how strategic acquisitions can transform industries when the deal rationale is clear, the integration preserves what made the target valuable, and the acquirer is patient enough to allow the investment to compound over time.

What made it work is instructive. Google paid a price that appeared expensive at the time but reflected a defensible thesis about long-term platform value. It preserved YouTube's brand and culture rather than absorbing it, and it identified the asset before competitors could. Speed and conviction in deal-making can be as important as analytical precision.

Frequently Asked Questions

What is M&A in business?

M&A stands for mergers and acquisitions, a term covering corporate transactions in which companies combine (merger) or one company purchases another (acquisition) to create value through synergies, accelerate growth, or reposition strategically. In business, M&A activity is used to enter new markets, acquire technology or talent, achieve economies of scale, or consolidate a fragmented industry. It is one of the most significant decisions a board and management team can make, involving complex financial, legal, and operational considerations.

What does M&A mean in finance?

In finance, M&A refers both to the category of corporate transactions and to the investment banking advisory practice that supports them. M&A advisory is one of the most prestigious areas of investment banking, involving valuation analysis, deal structuring, negotiation support, and the management of complex multi-party processes. When financial professionals refer to "M&A activity," they typically mean the volume and value of deal-making in a given period, a metric widely used as an indicator of corporate confidence, credit availability, and market valuations.

What are the main types of mergers and acquisitions?

The main types of M&A transactions are: horizontal mergers (between companies in the same industry), vertical mergers (between companies at different stages of the supply chain), conglomerate mergers (between companies in unrelated industries), acquisitions of control (where a buyer purchases a majority stake), and leveraged buyouts (where the acquisition is financed primarily with debt). Each type serves different strategic objectives and carries different integration challenges and regulatory considerations.

How is M&A valuation done?

M&A valuation typically uses three complementary methods. Discounted Cash Flow (DCF) analysis values the target based on its projected future cash flows discounted at an appropriate rate. Comparable company analysis (trading comps) benchmarks the target against similar public companies using multiples such as EV/EBITDA. Precedent transaction analysis (deal comps) examines valuation multiples paid in recent comparable M&A deals. Experienced deal teams present all three methods in a "football field" chart to establish a credible price range, rather than relying on a single method to determine value.

Why do mergers and acquisitions fail?

Research consistently shows that 70–90% of M&A transactions fail to deliver the financial returns projected at announcement. The most common causes are poor post-merger integration (systems, processes, and cultures that cannot be combined effectively), overpayment driven by competitive auction dynamics, unrealistic synergy estimates, loss of key management talent during the transition, and deals motivated by competitive pressure rather than a clear strategic thesis. Financial failure is often a symptom of strategic or cultural failure rather than a cause in its own right.

What is due diligence in M&A?

Due diligence in M&A is the structured investigation a buyer conducts on a target company before committing to final deal terms. It typically covers four parallel workstreams: financial due diligence (verifying earnings quality and identifying hidden liabilities), legal due diligence (reviewing contracts, IP, litigation, and regulatory compliance), commercial due diligence (testing the target's market position and growth assumptions), and operational due diligence (assessing systems, infrastructure, and management quality). Due diligence findings are used to validate the acquisition price, negotiate final deal terms, and identify integration priorities.