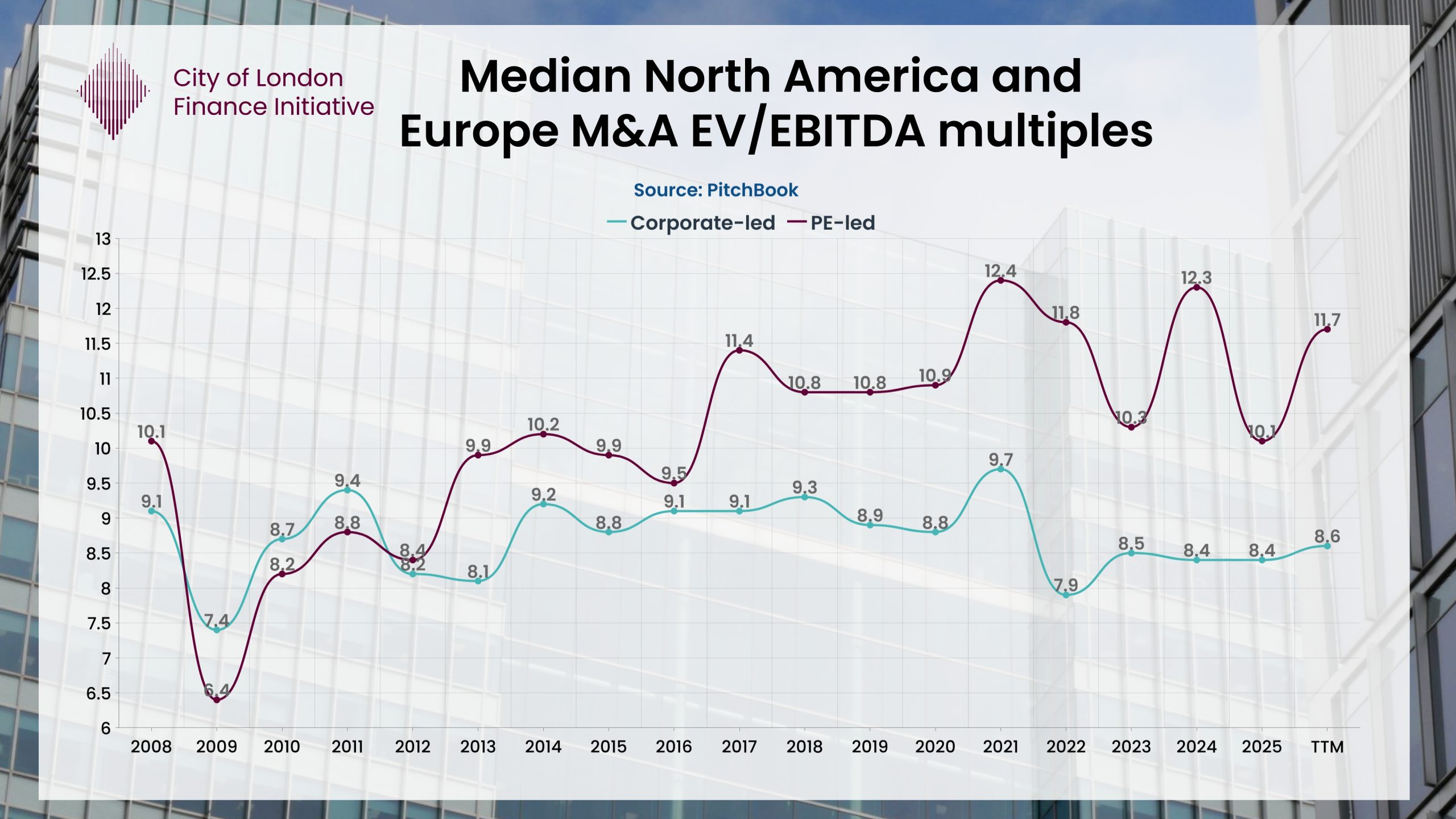

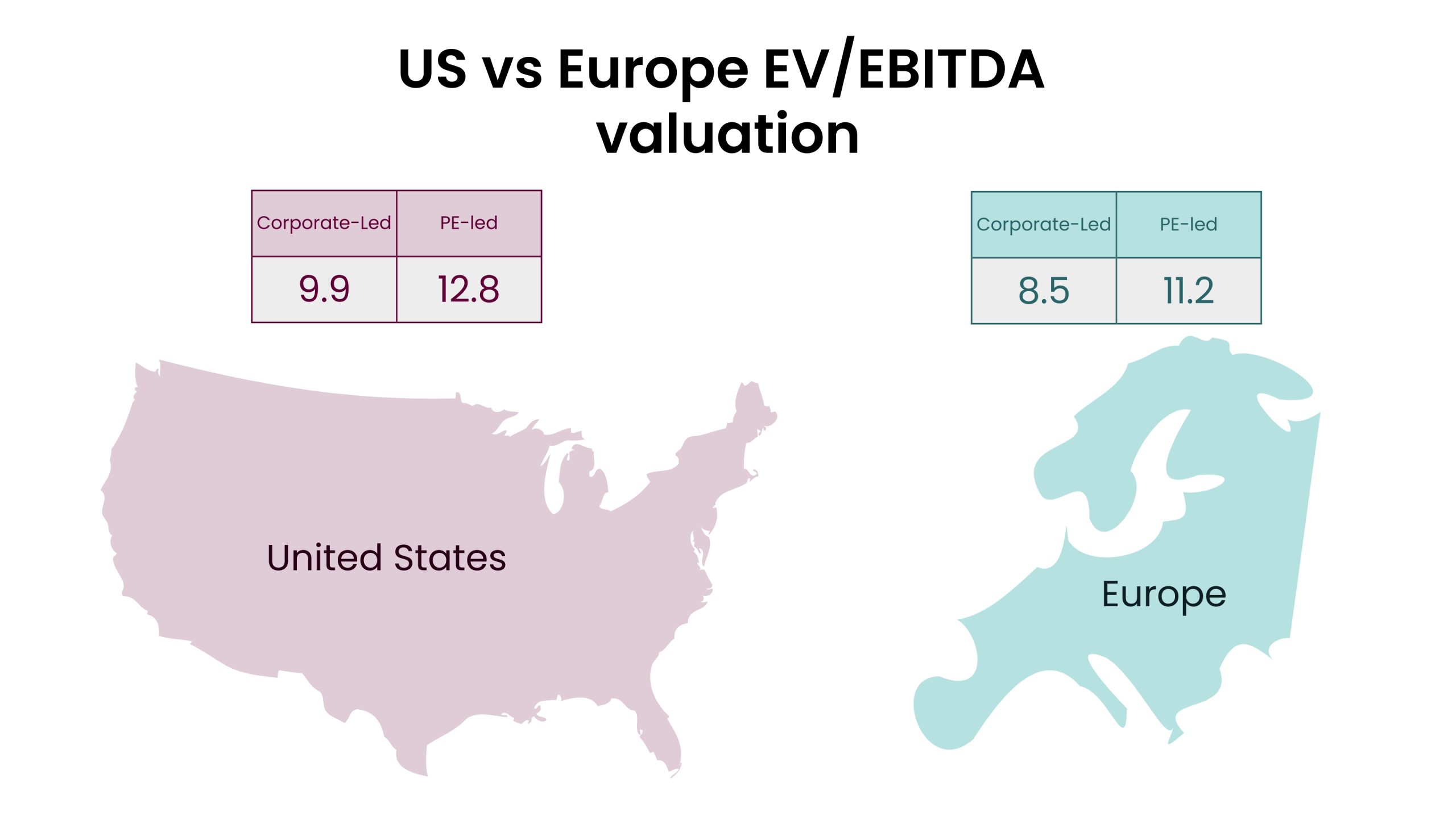

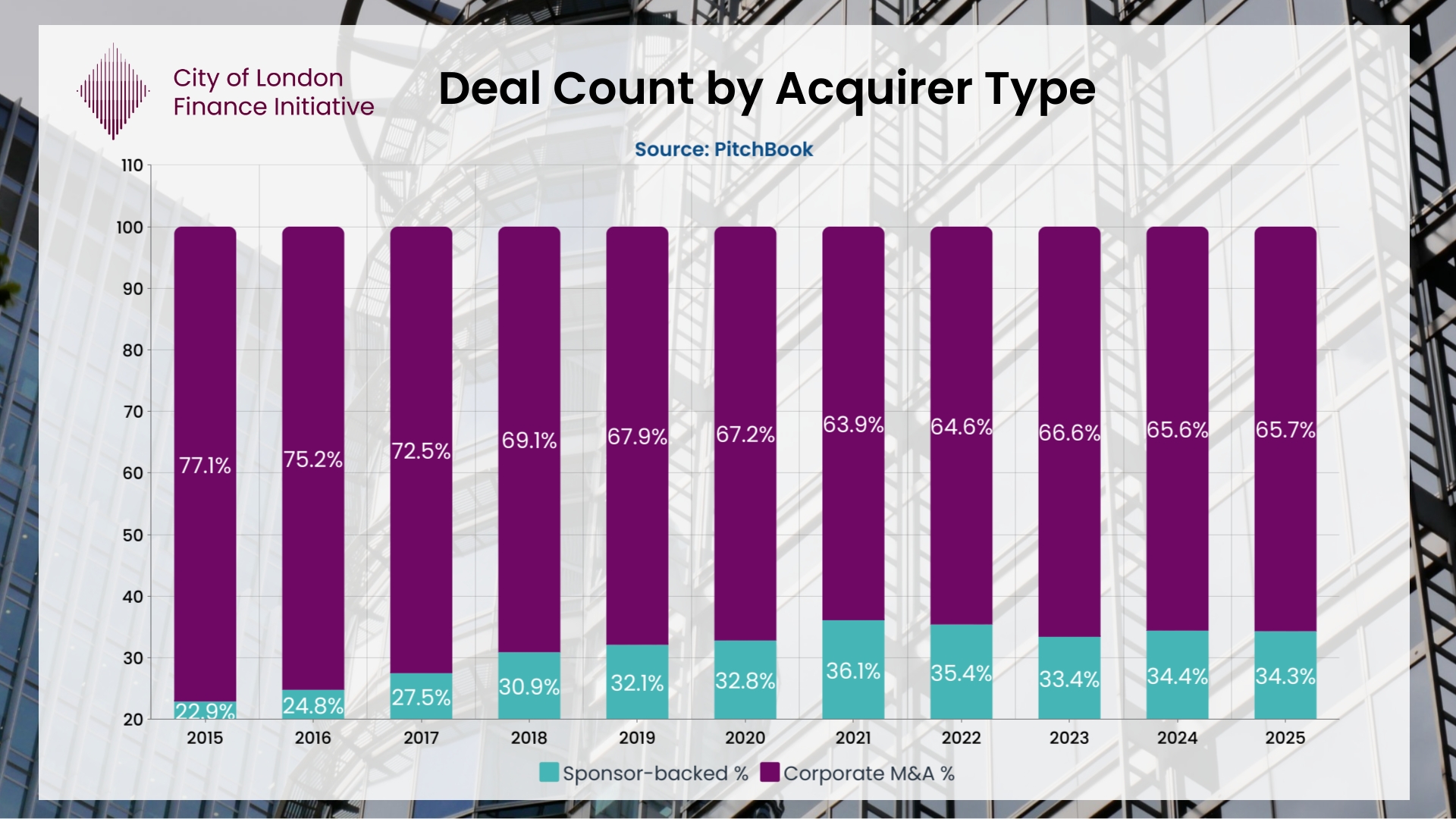

The pricing gap between buyer types mirrors this approach. As of Q2 2025, private equity buyers paid an average M&A EV/EBITDA multiple of 10.1x, compared to 8.6x for corporate acquirers.

Private equity firms typically underwrite acquisitions to meet internal rate of return (IRR) targets within a 4–7 year investment horizon. This structure allows them to justify paying higher entry multiples — particularly when they identify margin expansion levers, cost optimisation opportunities, or consolidation pathways to grow the asset.

For corporate acquirers, by contrast, the investment rationale is grounded in earnings increase, balance sheet discipline, and integration risk. These factors shape board-level decision-making and often cap how far valuations can stretch, even in cases of strong strategic alignment.

Another key factor behind this divergence is funding certainty. General partners with committed capital at Private Equity — even as dry powder ages — face deployment pressure. Corporate dealmaking, on the other hand, is more discretionary and often tied to annual cycles or long-term plans. This creates an urgency asymmetry that helps explain why private equity continues to outbid in many competitive processes.

Looking Ahead: What the Multiples Reveal

The ongoing private equity premium in deal valuations isn’t just about competition — it reflects how today’s market works. Private equity firms often need to invest within fixed timeframes, which gives them a different approach to risk. When capital must be deployed, there’s more willingness to pay higher prices, even if the exit options are unclear.

For corporate buyers, the situation is different. Their decisions are shaped by shareholders, credit conditions, and balance sheet limits — not fund deadlines. That’s why corporate valuations tend to stay more grounded, even when there’s a strong strategic case for a deal. In many ways, this gap between private equity and corporate buyers isn’t about who has the better strategy, but who is under more pressure to act.

What the data shows is that valuation multiples now reflect more than just sector fundamentals — they also depend on who the buyer is and how they’re funded. For sellers and boards considering offers, this matters. Understanding the difference between private equity and corporate logic can be just as important as the headline price. The gap between those bids isn’t only about today’s value — it shows how capital, strategy, and timing are shaping the future of M&A.

Explore Further from CLFI Insight

References:

- PitchBook, Q2 2025 Global M&A Report. Read more

- The critical role of exit readiness in today’s private equity landscape.