Other Matter Paragraph: What It Is and When It Appears

An Other Matter paragraph in an auditor’s report flags matters outside the financial statements. Learn when auditors include it and what it means.

Emphasis of Matter Paragraph: What It Means in Audit

An emphasis of matter paragraph draws attention to a key disclosure in the financial statements without modifying the auditor’s opinion. Here’s what it means.

Unmodified Audit Report: Definition and Meaning

An unmodified audit report means the auditor found no material misstatements. Learn what it contains, how it differs from modified opinions, and why it matters.

What Is a Qualified Opinion? Definition and Meaning

A qualified opinion means financial statements are true and fair except for a specific issue. Learn the causes, types, and what it means for boards and investors.

Disclaimer of Opinion: Meaning in Auditing

A disclaimer of opinion means the auditor cannot form a view on financial statements. Learn when it’s issued, why it matters, and what boards must do.

Adverse Opinion: What It Means in Auditing

An adverse audit opinion means the auditor concludes financial statements do not give a true and fair view. Here’s what it means and why it matters.

Qualitative Materiality: Definition, Factors and Examples

Qualitative materiality explains why a small figure can still be material. Covers the key qualitative factors auditors apply beyond numerical thresholds, with worked examples.

Quantitative Materiality: How Auditors Calculate Thresholds

Quantitative materiality is the numerical threshold auditors use to judge whether a misstatement is significant. Explains benchmarks, percentages, and worked examples.

What Is Materiality in Audit?

Materiality in audit is the threshold above which misstatements are judged significant enough to affect financial statement users. Explains how thresholds are set and applied.

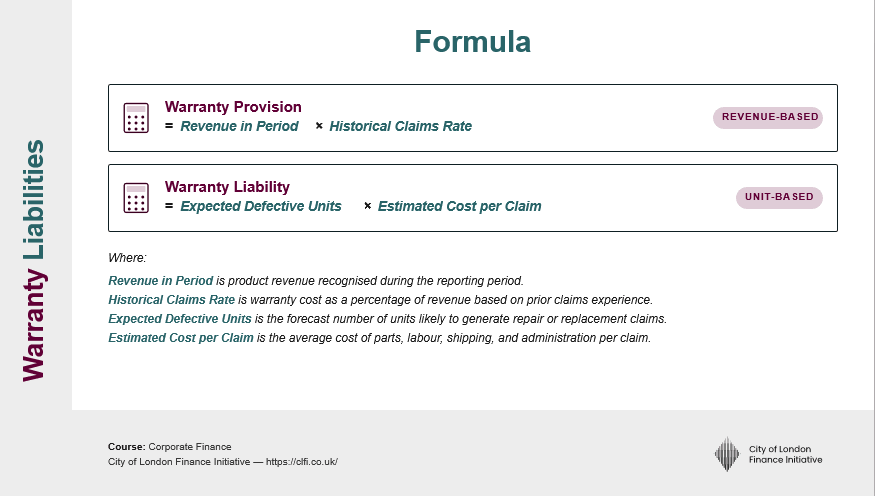

Warranty Liabilities: Definition and Accounting Treatment

What warranty liabilities are, how they are recognised under IFRS, how to calculate them, and why they matter in financial analysis and M&A valuation.