EBITDA is one of those finance terms widely used in company reports, investment pitches, and news articles about businesses. It stands for Earnings Before Interest, Taxes, Depreciation, and Amortisation. EBITDA provides a view of how much profit a company generates from its underlying business activities, before the impact of financing choices, tax regimes, or accounting charges related to the gradual use of assets. In this article, we set out what EBITDA represents, why it is widely used in financial analysis, how it is calculated in practice, and the limitations to bear in mind when relying on it.

The role of EBITDA as an analytical measure, and its distinction from cash flow and accounting income, is examined within the Business Valuation Executive Course.

Table of Contents

- What Is EBITDA?

- Why EBITDA Matters

- Breaking Down the Parts of EBITDA

- How to Calculate EBITDA

- Worked Example: EBITDA in Practice

- Common Adjustments to EBITDA

- Limits of EBITDA

- Further Reading

What Is EBITDA?

EBITDA is commonly used as an indicator of a company’s operating performance. It removes the effects of financing decisions (interest), differences in tax regimes (taxes), and accounting charges for the gradual consumption of assets (depreciation and amortisation). The result is a clearer picture of earnings generated by the company’s core operations. While it is often viewed as a proxy for “cash profit from operations,” it is not the same as actual cash flow.

Why EBITDA Matters

EBITDA has become a popular shortcut for comparing companies. Investors use it to judge profitability across industries and borders, because it removes differences in tax rates and financing. Lenders use it to test whether borrowers can service debt, often by setting covenants such as “Debt/EBITDA must stay below 3.” Companies highlight it in presentations because it often shows a cleaner, sometimes stronger, picture of performance than net income. Journalists and analysts use it in valuation multiples like EV/EBITDA to say what price investors are paying for each unit of profit.

Breaking Down the Parts of EBITDA

Each element of EBITDA reflects an adjustment made on the way from revenue to net profit:

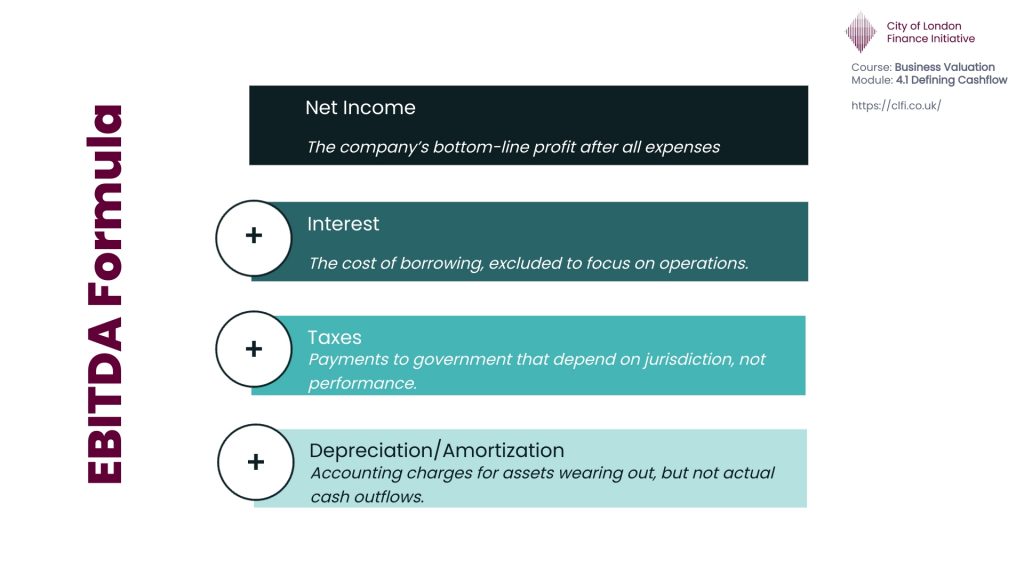

- Earnings: Refers to operating profit, often called EBIT. It begins with revenue and deducts routine operating costs such as wages, materials, and utilities.

- Interest: Represents the cost of borrowing. EBITDA excludes this to allow comparison between companies regardless of their capital structure.

- Taxes: Corporate tax charges vary by jurisdiction. By removing them, EBITDA highlights performance before the impact of local tax policy.

- Depreciation: A non-cash expense that allocates the cost of tangible assets such as buildings, machinery, and vehicles over their useful lives.

- Amortisation: Similar in concept to depreciation, but applied to intangible assets such as patents, trademarks, and acquired goodwill.

By excluding interest, taxes, depreciation, and amortisation, EBITDA isolates the profitability of a company’s core business operations. This is why in business valuation domain, this is also known as the closest metric to Free Cash Flow.

How to Calculate EBITDA

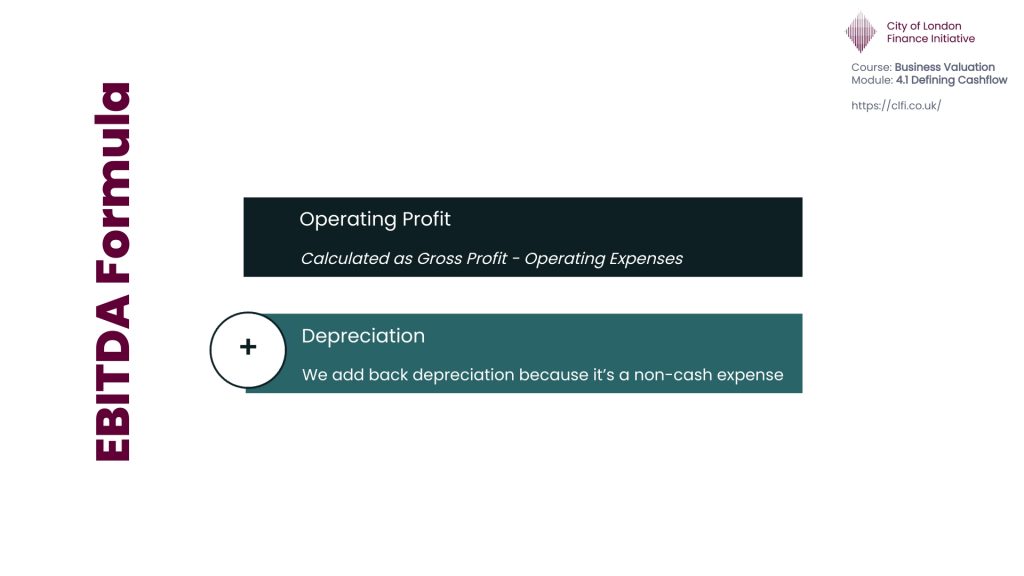

The simplest way to get EBITDA is to start from operating profit (also called EBIT) and add back depreciation and amortisation:

EBITDA = Operating Profit + Depreciation + Amortisation

Source: CLFI

Another way is to start from net income and add back interest, taxes, depreciation, and amortisation. Both approaches should give the same result if the numbers are consistent.

Source: CLFI